Why Your Big Online Casino Win Gets Frozen – Source-of-Funds Checks Explained

Why Your Big Online Casino Win Gets Frozen – Source-of-Funds Checks Explained

You hit a five-figure win, request the withdrawal, and instead of a payout confirmation you get a message asking for three months of bank statements. The balance sits there, locked. It feels like being accused of something. It isn’t.

Here is the first thing to understand, because almost every guide gets it wrong: the win didn’t trigger the freeze. Your pattern did. A source-of-funds request is a risk response, not a punishment, and the amount you won is only one of several signals that set it off — often not even the loudest one. Understanding what the casino is actually looking at is the difference between a 48-hour pause and a six-week ordeal.

This guide explains what trips the wire, which documents clear you fastest, how long it really takes, and — the part nobody tells you — why UK casinos have become so twitchy that they’ll now freeze a £400 cash-out that two years ago would have sailed through.

Two Different Checks Wearing the Same Costume

Most players think there’s one “verification” wall. There are two, they have completely different legal foundations, and they ask for nearly identical paperwork — which is exactly why the experience is so confusing.

The first is an anti-money laundering (AML) source-of-funds check. Its question is narrow and blunt: is this money clean? UK casinos are classed as Designated Non-Financial Businesses under the same global framework that governs banks, which means they carry a legal duty to confirm your stake isn’t the proceeds of crime. This obligation comes from the Money Laundering Regulations 2017 and the Proceeds of Crime Act, not from the gambling rulebook. Fail it and the operator must file a Suspicious Activity Report with the National Crime Agency — and they can’t tell you they’ve done so.

The second is a financial risk (affordability) check. Its question is different: can you afford this? This one lives in the Gambling Commission’s licence conditions and exists to catch gambling harm, not crime. Since February 2025, a light-touch version triggers at £150 in net deposits over a rolling 30 days, run quietly in the background using credit-reference data — no documents, usually no friction. An enhanced version, which does demand paperwork, kicks in at heavier loss thresholds: commonly around £500 net loss in 30 days or £2,000 in a year.

Why does the distinction matter to you? Because the documents that satisfy one don’t always satisfy the other, and knowing which check you’re facing tells you what to send. An AML check wants to see where a specific deposit came from. An affordability check wants to see that your income comfortably covers your play. A payslip answers both. A screenshot of a crypto wallet answers neither cleanly. Read the request carefully — the wording almost always reveals which animal you’re dealing with.

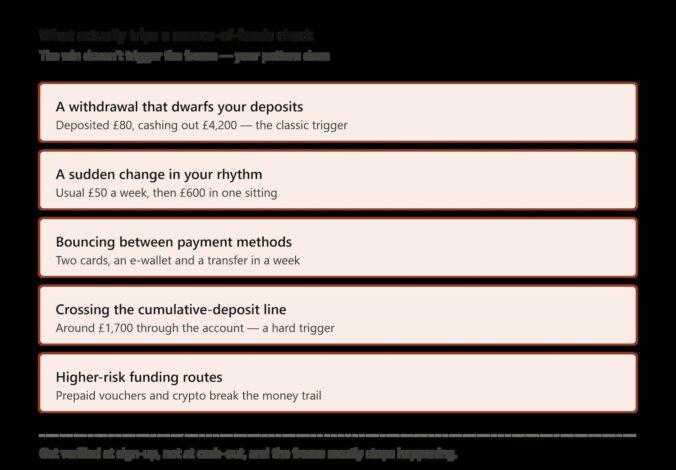

What Actually Trips the Wire

Forget the myth that there’s a magic number. There’s a cluster of behaviours, and the casino’s automated risk engine is watching all of them at once. Ranked roughly by how often they fire:

A withdrawal that dwarfs your deposits. This is the classic. You deposited £80 across the month and you’re cashing out £4,200. Nothing wrong with winning — but a payout that wildly exceeds what you put in is the single most reliable SoF trigger, because “deposit small, lose a little, withdraw clean winnings” is also a textbook laundering pattern. The engine can’t tell the two apart without looking.

A sudden change in your rhythm. You usually drop £50 on a Friday. This week you deposited £600 in one sitting. Velocity spikes flag harder than absolute amounts; a steady £600-a-month player attracts less scrutiny than someone who jumps from £50 to £600 overnight.

Bouncing between payment methods. Funding an account from two cards, an e-wallet, then a bank transfer inside a few days mirrors “layering” — the laundering step where money is shuffled to obscure its origin. If you split deposits across Neteller, a debit card and Trustly in a week, expect a closer look, however innocent the reason.

Crossing the cumulative-deposit line. UK casinos apply enhanced due diligence once you’ve moved roughly £1,700 (the £2,000-equivalent threshold from the regulations) through your account in linked transactions. This is a hard regulatory trigger, not a judgement call.

Higher-risk funding routes. The Commission has rated all crypto assets high-risk since February 2024, and prepaid instruments draw extra attention because they break the money trail — which is why a Paysafecard voucher, convenient as it is, can attract a source question that a debit card wouldn’t.

Notice what these have in common: not one of them is “you won too much.” The win is what makes you request the withdrawal that exposes the pattern. The pattern is what gets frozen.

Why Casinos Are So Twitchy Now

If verification feels more aggressive than it used to, that’s because it is — and there’s a specific, documented reason. The Gambling Commission has spent the last few years fining operators eye-watering sums for not checking source of funds, and the industry has responded by over-checking rather than risk another penalty.

The examples are instructive. In 2023, William Hill’s group paid £19.2 million — the largest enforcement payment in the regulator’s history at the time — and the findings read like a how-not-to manual: the operator failed to ask for source-of-funds evidence from a customer who staked £19,000 on a single bet, took no documentation from one who staked £39,324 and lost £20,360 in twelve days, and let another stake £276,942 while losing £24,395 over two months without a question. That is the behaviour the regulator decided was worth nearly twenty million pounds.

The direction of travel matters even more than the headline numbers. In December 2025, the operator of Betfred’s shops was fined £825,000 — its second action in two years — and the detail that should make every player sit up is why: the Commission ruled that triggering source-of-funds checks at £15,000 of losses or £125,000 of stakes over a year was set too high to be genuinely risk-based. Read that again. A £15,000 loss threshold was deemed too lax. The thresholds are being pushed down, hard, which is precisely why your modest win now meets a wall that a bigger one wouldn’t have a few years ago.

It isn’t isolated. ProgressPlay, which runs 134 white-label casino sites, paid £1 million in 2025 — a second offence — partly for failing to scrutinise source of funds. Across May to December 2025 alone the Commission took action against thirteen operators, and its compliance activity more than doubled year on year, with roughly one in four operators failing to reach a satisfactory standard. When the penalty for under-checking is a seven-figure fine and a possible licence review, and the penalty for over-checking is an annoyed customer, operators choose the annoyed customer every time. You are that customer. It’s not personal; it’s arithmetic.

Source of Funds vs Source of Wealth

A request will sometimes escalate from one to the other, and the words matter. Source of funds is about the specific money in play — this £5,000 deposit came from my salary, here’s the bank statement showing it land. Source of wealth is broader and more intrusive — how did you come to have money in the first place?

Picture depositing £50,000. A source-of-funds check confirms that particular fifty grand came from, say, a property sale rather than nowhere. A source-of-wealth check asks whether your overall financial picture — your job, your assets — makes a £50,000 deposit plausible at all. Source of wealth is reserved for genuinely high-value or high-risk cases and for politically exposed persons, and it’s where the paperwork gets serious: not just a statement, but evidence of how the wealth was generated. Most players will never see it. But knowing the ladder exists explains why a routine request can suddenly grow teeth if your answers don’t add up.

The Documents, Ranked by How Fast They Clear You

Not all evidence is equal. Some documents resolve a check in one pass; others invite a follow-up. From fastest to slowest:

Recent payslips (last one to three months). The gold standard for salaried players. They show regular, identifiable income and double as affordability evidence. If you’re employed and you’ve got them, send these first.

Bank statements (last three to six months). Reliable, but with a catch covered below. They want to see income arriving from a named source and the deposits to the casino leaving from the same account.

Self-employed evidence — an SA302, tax return, or business bank statements. Slower to assess because the reviewer has to interpret irregular income, but entirely acceptable. A dividend voucher or director’s remuneration statement works for company directors.

One-off windfall proof. Inheritance letters, a property-completion statement, a pension lump-sum confirmation, even a lottery-win receipt. These explain a deposit that your regular income obviously couldn’t — and if that’s the real story, providing it pre-empts the source-of-wealth question entirely.

A screenshot of a wallet or a crypto balance. The slowest and weakest. It shows money exists, not where it came from, so it almost always triggers a second request.

The redaction trap

You’re allowed to black out transactions unrelated to the check — the casino has a legal duty under UK GDPR to take only what’s necessary and not to keep it longer than needed. But there’s a sharp edge here that delays more cash-outs than any other single mistake: over-redaction. Black out so much that the reviewer can’t see your name, the account number, the incoming salary and the deposits to the casino, and they’ll simply ask again. Leave the four things they actually need visible — identity, account, income in, money out — and redact the weekly shop if you must. A clean, legible, in-date document that matches the name and address on your casino profile clears in one pass. A blurry phone photo of a folded statement with half the page hidden does not.

How Long It Actually Takes — and the Clock That Matters

Handled well, a source-of-funds check resolves in 24 to 72 hours once you’ve uploaded everything. Manual reviews, weekends and incomplete submissions stretch that.

But here’s the reframe that saves players the most grief: the payment rail is almost never the hold-up. Trustly can move your money in minutes; an e-wallet in hours. What you’re waiting on is the casino’s approval — the human or system signing off that your funds are legitimate and your bonus wagering is complete. The method is fast. The decision is the bottleneck. We’ve written separately about why the fastest-paying casinos win on approval speed, not payment speed, and source-of-funds is the single biggest reason an “instant withdrawal” turns into a three-day wait.

Your Rights While the Money Is Frozen

You are not powerless, and a good operator will respect this without being asked.

The casino must tell you a check is happening and, broadly, what triggered it — it can’t freeze your balance in silence. It must handle your documents under UK GDPR and bin them when they’re no longer needed. The check must be proportionate: a request for source-of-wealth-level evidence over a £200 cash-out is out of order, and you can say so. And if you believe you’ve been treated unfairly — unreasonable delay, disproportionate demands, a payout withheld without explanation — you can escalate to the operator’s Alternative Dispute Resolution provider, free, before you ever think about the Commission.

There’s one rule worth memorising, because it’s your strongest card. Since May 2019, a UK casino cannot withhold a withdrawal to demand a document it could reasonably have asked for earlier — at sign-up, say, rather than the moment you try to take winnings out. If a site let you deposit and play for months and only sprang an identity or source check when you tried to cash out a win, that delay may itself breach the licence conditions. Historically only about 15% of verification complaints involved documents demanded at the withdrawal stage, precisely because the rule exists to stop it.

The Get-Ahead Playbook

The single most effective thing you can do is refuse to be surprised. Almost every painful freeze traces back to a player who left verification until the worst possible moment — the moment they had money to lose by waiting.

Verify at sign-up, not at cash-out, while there’s nothing on the line and no incentive to rush. Upload your ID and a proof of address the day you register — and note that at a white-label network, that verification is shared across every sister brand, so being known on one site means being known on all of them. Players who do this routinely report withdrawals clearing in hours, because the slow layer is already done.

Keep your funding boring. Deposit from one account in your own name, and resist the urge to spread it across three methods in a week. A clean, consistent money trail is the fastest trail.

Match the paperwork to your profile before you’re asked. Know which document tells your story — payslip if you’re salaried, SA302 if you’re self-employed, a windfall letter if a one-off sum funded your play — and have a current copy ready. In date, legible, name and address matching your account.

And respond fast when asked. The clock only starts when you upload, and a casino that’s waiting on you is a casino that hasn’t approved your payout. Send the right documents, lightly redacted, in one go — and you turn a potential six-week saga back into the 48 hours it should have been.

A frozen win is rarely a sign you’ve done something wrong. It’s a sign the system is doing exactly what a decade of enforcement built it to do. Treat verification as a step you complete on day one rather than a wall you hit at the finish, and the freeze mostly stops happening to you at all. A frozen balance is usually temporary — but whether your money is safe if the operator itself fails is a separate question, covered in what happens to your balance if a casino goes bust. For more on how UK casinos handle money in and out, start with our online casinos hub.

FAQs About Source-of-Funds Checks

Is a source-of-funds check the same as an affordability check? No, though they feel identical. A source-of-funds check (AML law) asks whether your money is legitimate; an affordability check (gambling licence conditions) asks whether you can afford to play. Both can mean “send documents,” but they’re answering different questions.

Can a casino really freeze my winnings to ask for documents? Yes — UK-licensed operators are legally required to, when your activity triggers a check. What they can’t do is demand a document at withdrawal that they could reasonably have requested earlier, a rule in force since May 2019.

What’s the fastest document to clear a check? A recent payslip if you’re employed, because it proves regular, identifiable income and covers affordability at the same time. Self-employed players should lead with an SA302 or tax return.

Why is my withdrawal still pending after I sent everything? Almost always the casino’s approval stage, not the payment method — manual review, a bonus-wagering audit, or weekend processing. The money rail is fast; the decision is the bottleneck.

Can I black out transactions on my bank statement? Yes, transactions unrelated to the check. But don’t over-redact — leave your name, account number, incoming income and the deposits to the casino visible, or you’ll be asked again. Over-redaction is the most common cause of avoidable delay.

How long does a source-of-funds check take? Typically 24 to 72 hours once you’ve uploaded complete, legible documents. Incomplete submissions and manual reviews extend it.

Will using Paysafecard or crypto trigger a check? It can. Prepaid vouchers and crypto break the money trail, and the Commission has rated crypto high-risk since 2024, so both attract closer scrutiny than a debit card or bank transfer.

What happens if I refuse to provide documents? The casino is legally obliged to act — usually by restricting deposits or holding the withdrawal until the check is satisfied, and in some cases closing the account. Refusal doesn’t make the requirement go away.

Can I complain if I think the check is unfair? Yes. If a request is disproportionate or a payout is unreasonably delayed, raise it with the casino, then escalate free to its Alternative Dispute Resolution provider.

Does getting verified once cover me forever? Largely, but not absolutely. A casino can re-check if your details change or your activity shifts sharply — a sudden spike in deposits or a withdrawal far above your norm can prompt a fresh look even on a verified account.

18+. Play responsibly. Gambling can be addictive. For free, confidential support visit BeGambleAware.org or call the National Gambling Helpline on 0808 8020 133. This guide is general information, not legal or financial advice; individual casino procedures and regulatory thresholds can change, so check each operator’s current terms.

Written by: Jamie Shaw